Skip to content

Skip to content

If you are trying to find out what is a comparative market analysis, the answer goes far beyond reading basic online estimates or checking neighborhood asking prices. Many homeowners assume their property’s value matches whatever numbers an algorithm shows online.

However, true real estate pricing requires a meticulous analysis of actual localized market behavior.

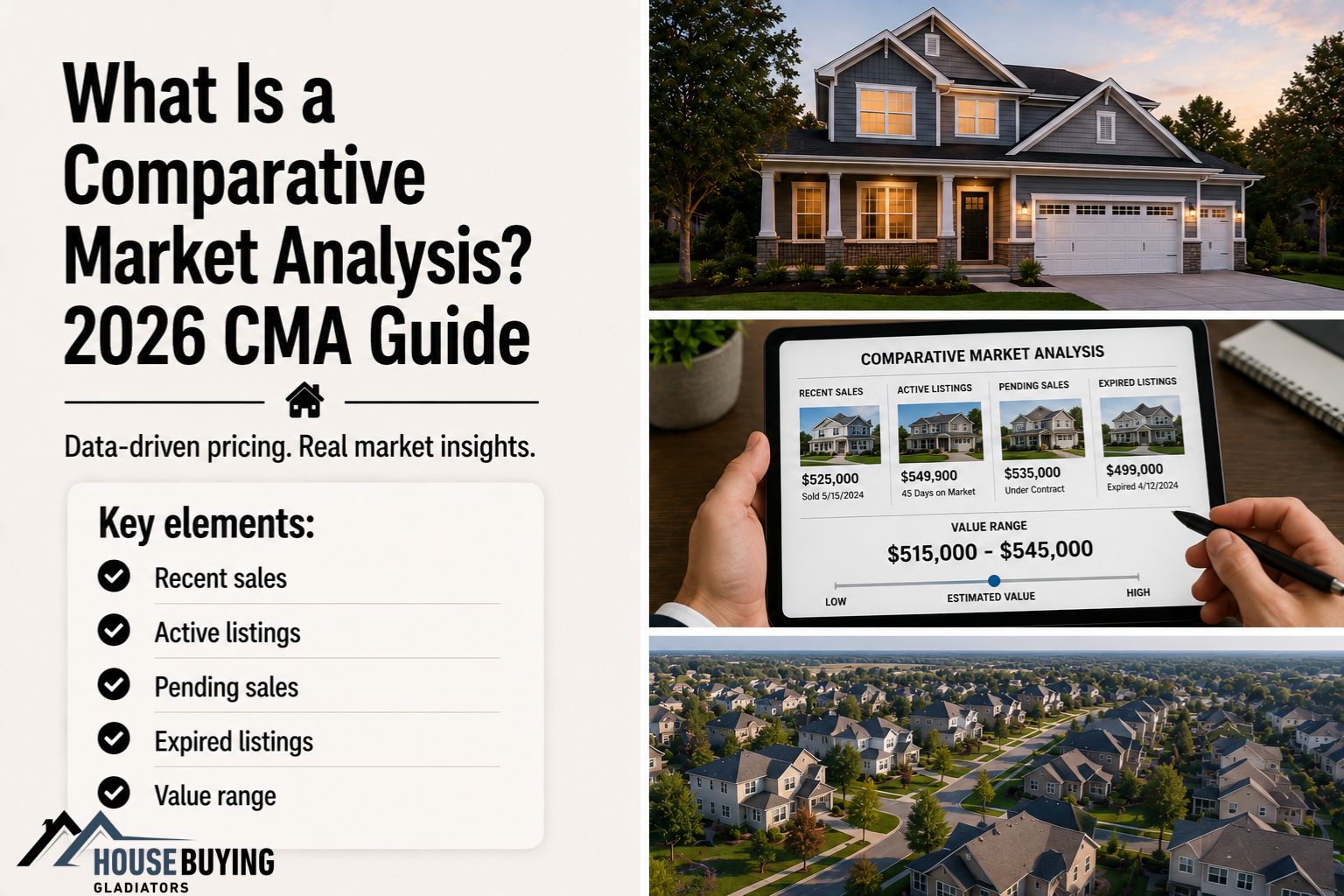

A comparative market analysis (CMA) is a detailed, data-driven report that estimates a property’s market value. It looks closely at similar homes that recently sold, are currently active, are pending sale, or failed to sell within your immediate neighborhood.

Instead of generating one fixed number, a properly built analysis calculates a realistic valuation range. Understanding what is fair market value of a home can also help homeowners build a more realistic pricing strategy before listing a property.

Comparative Market Analysis (CMA) Adjustment Simulator

CMA Property Adjustment Simulator

See how real estate agents balance market data to pinpoint true market value

1. Subject Property (Your Home)

2. Comparable Property (Sold Neighbor)

Comp #13. Live CMA Adjustments Ledger

Parsing a Comparative Market Analysis vs. a Formal Bank Appraisal

Understanding what is a comparative market analysis requires looking at how a real estate agent's pricing report stacks up against an official appraisal document. They fulfill entirely different roles in a transaction.

| Real Estate Report Characteristic | Comparative Market Analysis (CMA) | Certified Bank Appraisal |

| Primary Creator | Licensed Real Estate Agent or Broker | State-Certified Independent Appraiser |

| Core Objective | Establishing a competitive listing strategy | Underwriting mortgage financial risk |

| Data Methodology | Flexible tracking of active, pending, & sold data | Highly regulated parsing of historic closed sales |

| Primary Audience | Property sellers and home buyers | Mortgage underwriting teams and lenders |

| Report Payout Impact | Helps capture top-of-market initial offers | Places a firm ceiling on the buyer's loan size |

As this comparison shows, a pricing analysis functions as a flexible marketing asset, while an appraisal serves as a formal legal check for the bank. Homeowners who are still establishing a baseline value may also benefit from learning how to determine home value before comparing these valuation methods.

Additionally, inherited properties can create unique valuation challenges. If you are handling an inherited estate where property values must be legally split among family members, see this walkthrough on navigating partition lawsuits and forced home sales.

The Core Variables Used to Build What Is a Comparative Market Analysis

Real estate professionals rely on four distinct property buckets to build an accurate local market snapshot.

Closed Sales Baselines ➔ Active Competitor Tracking ➔ Pending Transaction Speed ➔ Expired Listing Warnings

Analyzing Closed Neighborhood Transactions

Recently closed sales establish the baseline value for your home. They show exactly what buyers recently paid for properties with similar square footage, age, and layouts.

These comparable sales also form the foundation of many of the valuation methods discussed in our guide on how much is my house worth.

If unrecorded encumbrances or boundary disputes complicate your neighborhood data, view this guide on resolving unrecorded easements on home titles.

Tracking Active Competition and Expired Listing Trends

Active listings show who you are competing against for buyers right now. However, these asking prices are simply seller expectations until a contract is signed.

Conversely, expired listings reveal where sellers made pricing mistakes, causing their properties to sit on the market until the listing agreement expired. Understanding what lowers property value can also help homeowners avoid some of these common pricing errors.

If you are trying to price your property to avoid foreclosure and need a quick transition strategy, review our advice on structuring a pre-foreclosure short sale strategy.

Why Online Estimators Cannot Replace What Is a Comparative Market Analysis

When evaluating what is a comparative market analysis, remember that automated online platforms cannot substitute for direct human market expertise.

[Public Tax Records] + [Basic Zip Code Algorithms] - [Real Interior Inspection Data] = Faulty Valuation Estimates

Online property estimators run entirely on computerized mathematical models. They analyze broad public records across entire zip codes but cannot evaluate interior condition, functional layouts, or premium upgrades.

An experienced agent can manually adjust for local variations that algorithms often miss. This human analysis also helps account for many of the factors discussed in our guide on what adds value to a house.

Additionally, inaccurate or outdated ownership records can sometimes affect public data. If your property records are cluttered with old ownership clouds that interfere with automated estimates, see our guide on how quiet title actions clear property records.

How Adjustments Protect Sellers From Expensive Overpricing Errors

A property value calculation is never a simple guessing game. It requires making adjustments for every meaningful difference between your home and the comparable properties being analyzed.

Comp Sale Price ➔ Subtract Value for Comp Upgrades ➔ Add Value for Subject Advantages ➔ Adjusted Pricing Target

For example, if a comparable home sold for a premium because it had a fully updated kitchen or an additional bedroom, the professional preparing the report may adjust that property's sale price accordingly. This process helps ensure the comparison remains balanced.

These adjustments also help homeowners avoid setting unrealistic asking prices that may discourage buyers. Additionally, understanding how much they may actually make selling their house can provide useful context, since pricing decisions directly affect net proceeds.

If you want to understand how contracts can protect buyers and sellers during these negotiations, review our breakdown of essential real estate contract financing contingencies.

Frequently Asked Questions

It is a pricing report built by an agent that estimates a home's value range by comparing it to similar nearby properties.

Licensed real estate agents and brokers create these reports to help sellers pick a list price and help buyers write competitive offers.

No. An agent builds a CMA to plan a marketing strategy. A state-certified appraiser creates an appraisal to clear a buyer's mortgage loan.

Most local real estate agents offer a pricing analysis for free as a regular part of their initial listing presentation.

Agents focus on transactions that closed within the past 90 days. They turn to older data only when looking at highly unique properties.

You can look up public records online, but agents have direct access to the MLS database, which tracks pending and expired listings.

A report is typically reliable for 30 to 60 days. After that window, new neighborhood sales and moving interest rates change the market.

Agents choose different comps and apply different values for updates. This variation is normal and usually leads to a similar overall pricing range.

No. Computer algorithms cannot check home condition, evaluate layout functionality, or adjust for minor neighborhood boundary nuances that affect final sales.

Assuming the report guarantees an exact final sales price. A pricing report outlines a realistic target range; buyer demand decides the final payout.

Conclusion: Build an Objective, Data-Driven Pricing Foundation

Answering what is a comparative market analysis requires looking past personal attachments and focusing on local market data. Grounding your pricing strategy in recent neighborhood transactions protects you from costly listing delays down the road.

Ready to see how property updates adjust a home's value? Scroll back to the top of this guide to run your property numbers through our interactive adjustments simulator. If you want to see exactly how listing values are verified once you accept an offer, review this master guide on how title insurance companies verify property ownership.