Skip to content

Skip to content

If you are trying to understand what is fair market value of a home, the true answer goes far beyond automated online estimations or personal expectations. Many property owners assume their initial asking price reflects true market worth.

However, real estate valuations are determined by objective market forces rather than emotional investments.

Fair market value represents the exact price an asset shifts ownership for under open, competitive real estate conditions. Both parties must be fully informed, acting in their own self-interest, and under absolutely no outside pressure to close the deal.

To determine this baseline number, you must look at objective transactional data rather than assumptions or emotions. This is also why many homeowners first learn how to determine home value before setting realistic pricing expectations.

Fair Market Value Adjustments Estimator

Fair Market Value Adjustments Estimator

Evaluating Fair Market Value vs. Alternative Housing Benchmarks

Answering what is fair market value of a home requires separating open-market data from specialized municipal tax or lending figures. These numbers rarely match.

| Real Estate Valuation Metric | Primary Data Source | Primary Practical Use Case | Impact on Your Payout |

| Fair Market Value (FMV) | Open Market Supply / Demand | Setting competitive listing targets | Maximizes final buyer offers |

| Assessed Tax Value | County Assessor Public Records | Computing local annual property taxes | Determines recurring annual carrying costs |

| Appraised Bank Value | Independent Certified Appraisers | Underwriting traditional mortgage risk | Caps the buyer’s maximum loan size |

| Distressed Investor Value | Net Equity Minus Overheads | Accelerating immediate cash liquidations | Eliminates structural repair liabilities |

As this dataset proves, a single property can carry drastically different valuations simultaneously depending on who is pulling the data. Homeowners can also benefit from understanding how much is my house worth, since different valuation methods often produce different results.

Additionally, certain financial situations may require specialized tax planning. If you are dealing with a complex financial settlement or looking to preserve equity from future property sales, check out this guide on navigating home capital gains tax exclusions.

The Core Elements Used to Determine What Is Fair Market Value of a Home

Real estate professionals analyze four primary variables to figure out exactly what a property is worth on the open market.

Verify Local Comps ➔ Adjust for System Wear ➔ Factor Inventory Pressure ➔ Compute Final Fair Market Value

Analyzing Recent Hyper-Local Comparable Sales

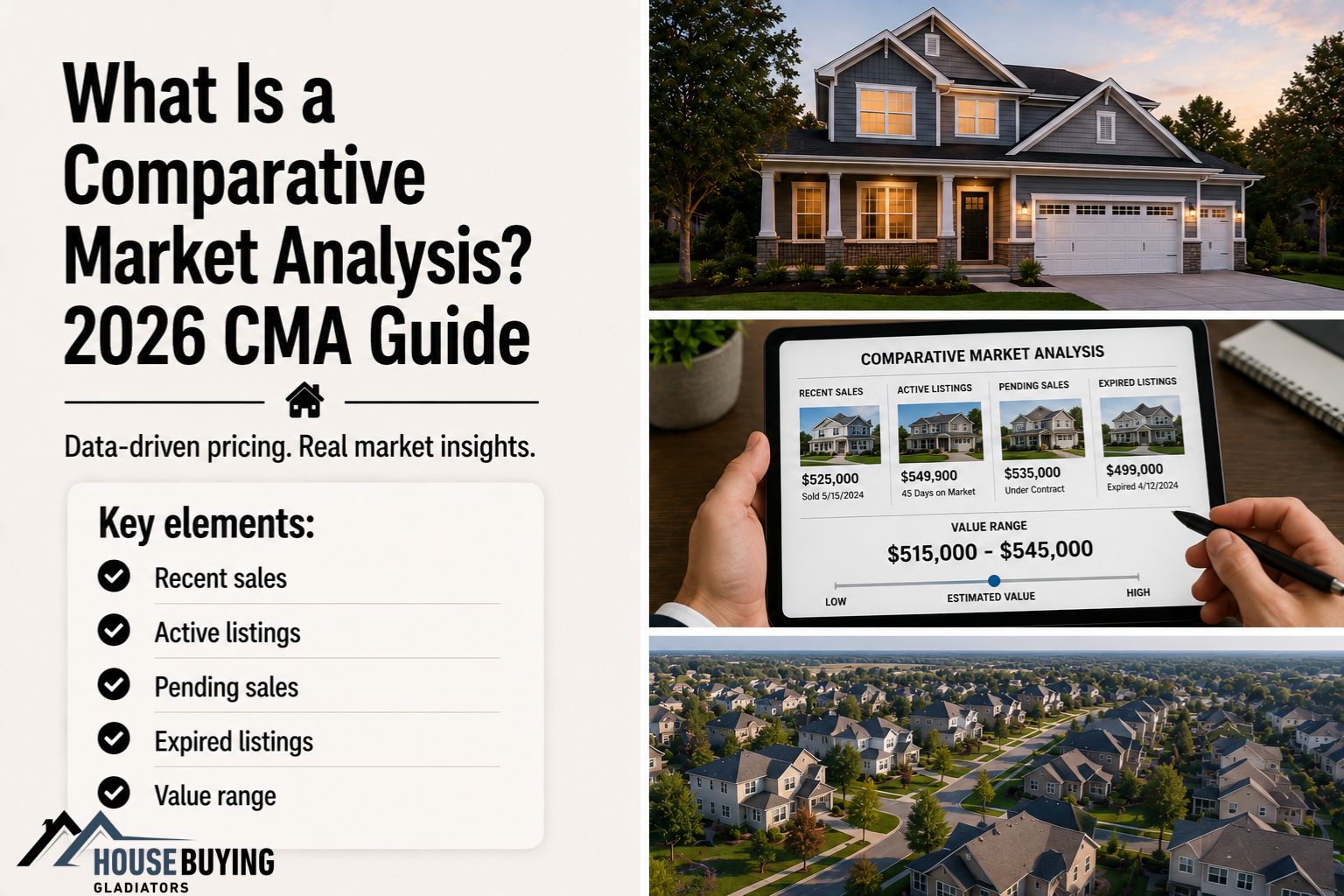

Recent comparable sales, or “comps,” form the absolute foundation of property valuation. These same comparable sales also play a major role in comparative market analyses, which agents frequently use to establish pricing strategies. Appraisers look at closed transactions within your immediate neighborhood over the past 90 days.

They compare square footage, lot size, bedroom counts, and overall layout functionality. If you are tracking comps for unique properties or income-producing units rather than standard single-family layouts, read this walkthrough on valuing duplexes and multi-family real estate.

Accounting for System Wear and Deferred Maintenance

Sellers often assume remodeling costs convert directly into added home value dollar-for-dollar. However, many of these same factors are discussed in our guides on what adds value to a house and what lowers property value. However, buyers look closely at structural risk windows instead.

An aging roof, a failing HVAC system, or outdated electrical components cause buyers to lower their offers to cover future capital expenses. If your neighborhood properties struggle with hidden environmental factors like clay soil shifts or high water tables, review our advice on how foundation damage impacts market value.

Why Automated Online Property Estimators Are Frequently Inaccurate

When researching what is fair market value of a home, relying solely on online evaluation tools can skew your pricing strategy. Algorithms are naturally blind to localized nuances.

[Public Tax Records] + [Basic Zip Code Algorithms] - [Real Interior Inspection Data] = Faulty Valuation Estimates

Online valuation models pull their numbers from raw public data feeds and historical title transfers. They cannot see high-end kitchen remodels, premium interior upgrades, or underlying foundation settlement issues.

Consequently, these automated values can miss the true market mark by tens of thousands of dollars. If your home sits on a uniquely shaped lot or borders commercially designated parcels, read this deep dive on how municipal zoning laws affect property value.

How Changing Market Inventory Shifts True Property Valuations

A house does not exist in a vacuum. External economic forces alter buyer behavior and shift property values without any changes being made to the home itself.

Rising Mortgage Rates ➔ Compressed Buyer Budgets ➔ Expanding Local Inventory ➔ Softening Fair Market Value

During a competitive seller’s market with low inventory, multiple buyers bid against each other, driving fair market value upward. Conversely, when mortgage rates rise, buyer purchasing power shrinks, causing local inventory to sit on the market longer. This shift gives buyers more negotiating room to demand price drops. To protect your sale timeline from crashing due to these sudden shifts in inventory, view this comprehensive strategies on selling a house in a buyer’s market.

Frequently Asked Questions

It is the price an informed buyer and an independent seller agree on in an open, competitive market, without any outside pressure to close.

The open market itself determines value. Buyers, sellers, appraisers, and real estate agents analyze comparable data to estimate this ever-changing target number.

No. Local county tax assessors use automated public records to calculate property taxes. This number is typically lower than open market values.

Each online platform uses its own unique algorithm, updates its data on a different schedule, and weights neighborhood boundary lines differently.

No. Home renovations rarely yield a 100% return. Upgrades improve buyer demand but do not automatically raise value by what you paid.

Yes. Mortgage appraisers follow strict bank guidelines. If local neighborhood comparable sales do not support your contract price, an appraisal gap occurs.

Professionals prioritize home sales that closed within the past three to six months. They avoid older data because market conditions shift quickly.

Higher interest rates increase monthly mortgage payments. This compresses buyer budgets, cools overall demand, and puts downward pressure on home values.

Hire a local licensed appraiser or ask an experienced real estate agent to put together a comprehensive comparative market analysis (CMA).

Yes. Excellent curb appeal sets a strong first impression. It reduces perceived buyer risk and helps you secure top-of-market offers faster.

Conclusion: Build an Objective, Data-Driven Pricing Foundation

Understanding what is fair market value of a home requires looking past personal attachment and focusing on local market data. Grounding your pricing strategy in recent comparable sales can help you avoid costly pricing mistakes.

Homeowners who also understand how much they may actually make selling their house are often better prepared to build realistic financial expectations, since property value directly affects net proceeds.

Ready to see how your home’s condition may influence its value? Scroll back to the top of this guide to use our interactive valuation adjustments calculator.

If you are preparing for a professional valuation, review this checklist for documenting home improvements for an appraiser before scheduling an appraisal or walkthrough.